Clark Packard and Chad Smitson

A recent NBER working paper by Chang Ma and Shang-Jin Wei titled “The Chinese Current Account Imbalances: Puzzles, Patterns, and Possible Causes” investigates the causes of China’s current account surplus and challenges some widely held assumptions in the process. Conventional wisdom attributes China’s persistent current account surplus primarily to its industrial policy and export subsidies. The authors of the new paper push back on that narrative. While industrial policy may shape outcomes in individual sectors, it leaves the aggregate current account essentially unaffected. The true drivers, the authors argue, are structural macroeconomic forces—demographics, financial repression, and a deteriorating property market—that have persistently elevated China’s savings rate relative to its investment, producing a durable external surplus.

First, the authors argue that China’s industrial / trade policy has a muted impact on its current account. Their main line of reasoning is the Lerner Symmetry Theorem, which essentially postulates that given high-to-full employment, “a tax on imports is a tax on exports,” because labor and resources must be pulled from other sectors to make up for the decrease in imported goods. The reverse is true for exports. Taken together, the authors argue and support with historical evidence that while trade policies may impact individual industries, they do not leave a mark on the national current account because economy-wide imports and exports tend to move together as a result. This insight aligns with the national accounting identity—a country’s current account balance is ultimately determined by the gap between national savings and investment, not by trade or industrial policy—a point Cato scholars have similarly emphasized in examining the persistent US trade deficit.

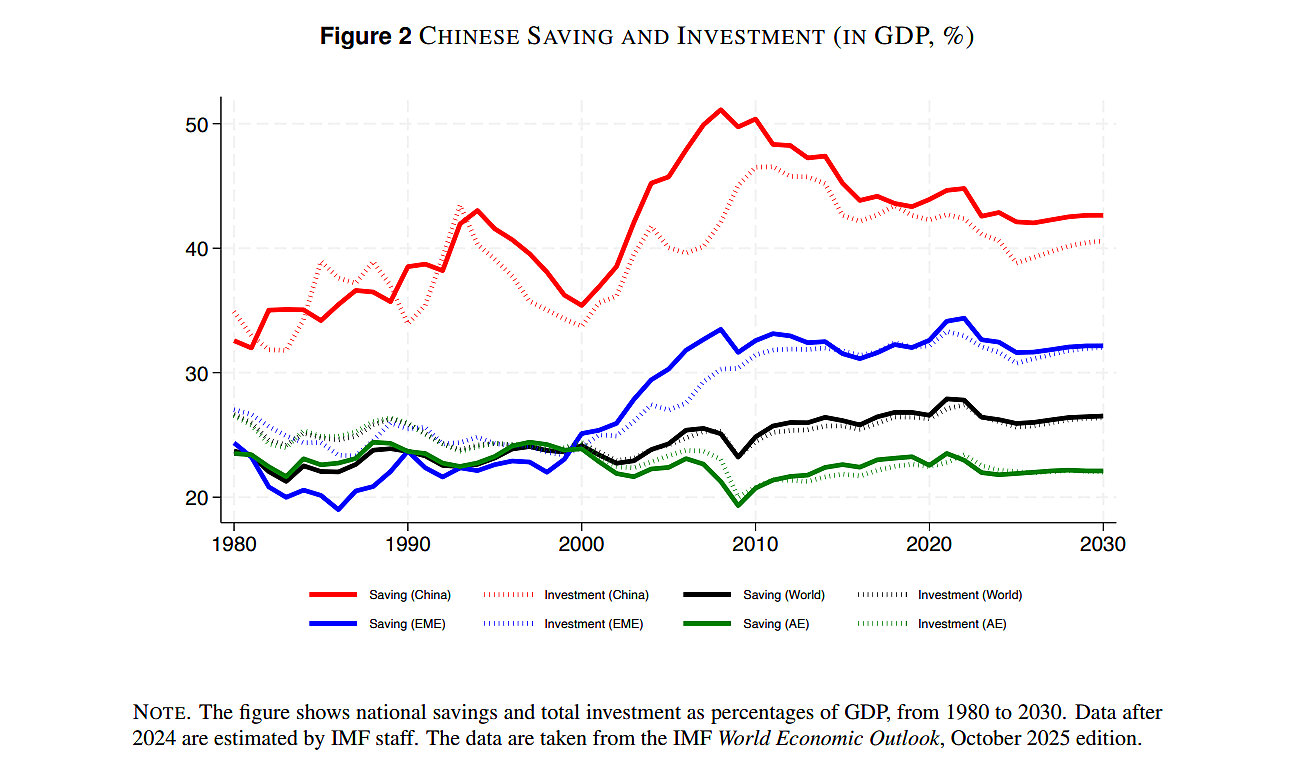

The following figure, featured in the paper, shows that China pairs a very high investment rate with an even higher savings rate, each exceptional by global standards. This combination suggests that its surplus reflects deeper structural factors rather than weak domestic investment or trade policy.

So, what drives China’s consistently elevated surplus? The authors identify three structural factors: an unusual demographic profile, a deeply distorted financial system, and a collapsing property market. Due to the impact of the One Child Policy, China has a distinctly male-skewed sex ratio. The results of this, the authors show, are fourfold: first, the marriage market is highly competitive due to the surplus of men and shortage of women. Therefore, men (and parents of young men) are highly incentivized to build up their savings to make themselves as financially attractive as possible to prospective partners. Second, the generational effect of having many people come of working age can raise the savings rate. Third, simply having fewer children leads parents to save more of their income. The authors cite a study indicating this alone increased the savings rate by 7 percentage points between 1970 and 2009. Fourth and finally, parents are incentivized to build up their own savings because they cannot depend on more than one child in their retirement and old age. The authors estimate that this factor alone may account for roughly half of China’s increase in the savings rate over that period.

China’s savings rate and, subsequently, its current account are also greatly affected by its poorly functioning financial system. The authors argue that because the banking system disproportionately favors state-owned firms, non-state, high-growth firms are crowded out of access to capital. The result is one of the world’s highest corporate savings rates. Firms and households must build up their own savings or seek foreign investment, further increasing China’s current account deficit.

Finally, China’s weak housing market has eroded household wealth, weakening aggregate demand to the point of a deflationary economy. Import demand has followed suit, providing yet another mechanical boost to the current account.

The authors conclude with their proposed policy implications:

Efforts to address China’s current account surplus need to take structural determinants seriously, rather than focusing solely on trade or industrial policies. While short-run macroeconomic stimulus aiming at addressing housing market weakness and deflation can help boost consumption and reduce trade surplus in the short run, policy reforms aiming at addressing structural factors underlying excess household and corporate savings are needed as part of a sustained long-term solution.

In light of comments filed by Cato’s Scott Lincicome and Chad Smitson in response to USTR’s Section 301 investigations, the new NBER working paper carries an important message: trade balances do not tell the whole story. The administration is attempting to assess foreign economies using broad, national-level macroeconomic indicators such as trade surpluses and excess capacity. However, as the authors of this paper have explored, these metrics are shaped by structural domestic forces—demographics, financial repression, and weak household demand—that tariffs cannot address.

As Cato scholars have documented for years, the US trade deficit is similarly a product of macroeconomic factors, the gap between national savings and investment, not unfair foreign trade practices. This paper is complemented by a recent piece by Maurice Obstfeld from the Peterson Institute exploring the myriad factors that influence the US current account, in particular its enduring fiscal deficit.

Prior US tariffs have shuffled bilateral trade imbalances around without denting the overall deficit. Policymakers who genuinely want to address trade imbalances need to grapple with the underlying reflexive reach for tariffs as a remedy.